A combination of changing consumer habits and live access to driving styles and conditions is transforming the automotive insurance business – with the support of OEMs. The consumer switch is away from physical insurance claims. In its Future of Claims report, Data, analytics and technology provider LexisNexis® Risk Solutions, says that prior to the pandemic, only 15% of U.S. auto insurance claims were handled virtually. Since the March 2020 shutdown, almost 100% of claims are now handled virtually.

The report predicts that auto insurance carriers will be able to move to touchless claims if they cater to their customers’ wants and needs when it comes to the digital claims experience.

Key highlights include:

• Comfort and satisfaction with the claims automation process is increasing, and consumers are now seeing the advantages of self-service claims, as 62% say it’s more convenient to submit a claim anytime/anywhere, and 55% say it enables faster claims settlement

• Younger, more technology-savvy generations are adopting faster as 68% of Millennials and 53% of Gen Xers say the pandemic has made them open to filing a claim online

• Mastering a hybrid model is the sweet spot as it provides the benefits of automated processing solutions combined with access to help from a claims representative when needed, which helps avoid frustration

• Automation has shifted from driving efficiency to driving decisioning as carriers are now leveraging the benefits of artificial intelligence and machine learning to enhance the processes for damage assessments, segmentation, estimations and payouts, in addition to intake support.

“While the past year has proven to be a great awakening for claims automation, we’re now at a crossroad, and what will set insurers apart is complete claims handling digital transformation and move from traditional to touchless,” said Bill Brower, Vice President of Claims, LexisNexis Risk Solutions in a media release.

“Overall, consumers are willing to move to more self-service claims options as long as the experience continues to evolve to meet their expectations and deliver the benefits of convenience and security.”

An important part of the future of automotive insurance is connected car technologies. In 2020, the company launched LexisNexis® Telematics OnDemand in the U.S., a solution that integrates telematics-based driving behavior data into insurer rating and underwriting workflows.

The solution is built to deliver telematics-driven scores and attributes based on participating LexisNexis® Telematics Exchange members.

The U.S. Telematics Exchange can ingest data from U.S. automakers, mobile apps, as well as third-party services.

After consenting to share their telematics data, the consumer may receive discounts on their insurance, participate in safe driving reward programs or tap into other value-added services.

Insurance carriers can leverage the driving information with no upfront monitoring period when quoting a consumer for their auto insurance. Insurers can use this information for risk segmentation, rating and pricing, ultimately to help improve loss ratios, reduce at-fault claims expenses and drive greater customer retention and loyalty.

In the U.S., LexisNexis Risk Solutions works with General Motors, Mitsubishi Motors North America and Nissan North America on a number of programs. The company has also built automotive OEM-specific solutions, such as LexisNexis® Recall Clarity. LexisNexis has also established a European connected car data exchange with a growing number of automakers.

Across the Atlantic, LexisNexis Risk Solutions was selected in November 2020 to become part of Project smashHit – a project funded by the European Union – to play a key role together with consortium the partner Volkswagen AG in enabling millions of consumers to benefit from connected car data.

The project coordinator is Institut für angewandte Systemtechnik Bremen GmbH ATB), which has deep knowledge in the research on car data as well as management of EU-funded projects.

The Project smashHit consortium is tasked with creating a secure platform that will increase consumer trust and confidence in personal connected car data sharing for specific use cases. LexisNexis Risk Solutions will lead the automotive insurance use case in partnership with Volkswagen AG.

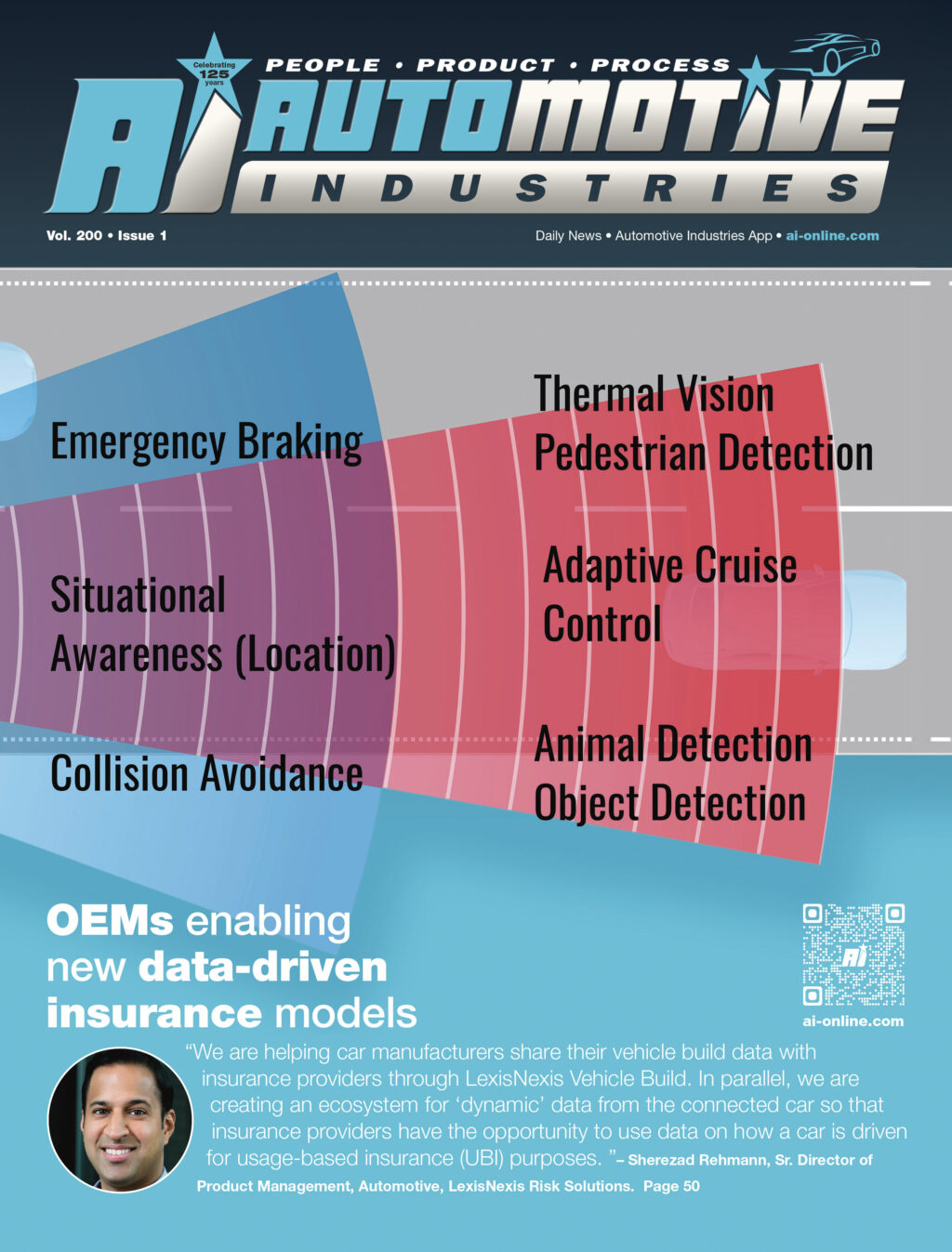

Another area of opportunity is with Advanced Driver Assistance Systems (ADAS), which was launched in the U.S. through LexisNexis® Vehicle Build. It offers the auto insurance industry better insight into what ADAS features a vehicle is equipped with and how those features impact risk. In the European market, the solution has been tested over the last year with the team having analyzed 2.7 million vehicles, readying it for launch in the near future.

Automotive Industries (AI) asked Sherezad Rehmann, Sr. Director of Product Management, Automotive, LexisNexis Risk Solutions, to tell us about the LexisNexis solution to use ADAS in the auto insurance industry.

Rehmann: It has been a challenge for insurers to identify exactly what ADAS features a specific vehicle is equipped with when writing a motor insurance policy because the data was not readily available to insurers or easily ingested into workflows.

Each car manufacturer has created unique terminology, definitions and naming structures – sometimes releasing multiple features within the same model year. In addition, many items are chosen as optional extras when a vehicle is purchased from new.

To address this challenge, we built an ADAS classification system for the insurance market. More than 2.7 million vehicles have been assessed across four European countries to understand how the specific ADAS fitted to a vehicle can impact insurance claims.

In addition to using ADAS data from third party vehicle data sources, European car manufacturers such as Mercedes-Benz Connectivity Services are now starting to share ADAS data with us, resulting in 80% coverage of the European market.

Using all the intelligence gathered over the past year, the confirmation of the safety features of a car, along with how well they perform is becoming accessible to insurance providers in Europe, at a Vehicle Identification Number (VIN) level for insurance quotes.

AI: How will connected car technologies change the insurance landscape?

Rehmann: ADAS data down to VIN-level from LexisNexis Vehicle Build and real-time driving data from the connected car can offer an additional layer of insight and added benefits to existing “proxies” used by motor insurance providers for calculating risk.

This offers the opportunity for drivers to be rewarded for the investment they have made in an ADAS-equipped car and their good driving habits through lower insurance premiums. Connected car data could also enable pay as you drive, pay how you drive and other mobility options.

We are helping car manufacturers share their vehicle build data with insurance providers through LexisNexis Vehicle Build. In parallel, we are creating an ecosystem for “dynamic” data from the connected car so that insurance providers have the opportunity to use data on how a car is driven for usage-based insurance (UBI) purposes.

The connected car data exchange will enable driving data from motor manufacturers to be brought to insurance providers in a normalized, contextualized and standardized manner. The ultimate goal is to deliver this as an actuarial grade driving score for UBI, regardless of the vehicle make, model or device type.

This approach removes much of the complexity, cost and provides confidence on compliance issues involved in delivering insurance benefits for the connected car. It also helps pave the way for new mobility models.

In the near future, we will see the evolution in ADAS features that have over-the-air update capabilities, giving the consumer greater flexibility and control. We are starting to work with our car manufacturer partners to evolve the LexisNexis Vehicle Build solution to best reflect these innovations.

More Stories

Auto Repair Services: Keeping Your Vehicle Road-Ready

Unleashing Creativity with Vidnoz: The Best Free AI Video Generator in 2025

The Connection Between Air Drying and Energy Efficiency in Industrial Settings