To use a motoring metaphor: any leader heading up a team in automotive manufacturing needs much more than a saloon car (no matter how fancy or powerful) to drive their way round, through and over the many challenges facing them. They are going to need a serious 4X4 and exceptional driving skills.

A tsunami of change has left behind a debris field that includes globally disrupted supply chains, confused consumers, increased focus on the environment, commoditization, labor, the entry of new digital technologies by companies which do not care much about traditional automotive industry norms, financial challenges and more. According to the team at the Deloitte Automotive Supplier Practice, component suppliers will be the first to feel the impact of electrification. Drive train components make up around one-third of the material costs for a standard volume internal combustion (ICE) car. Most of these components are not needed in electric vehicles. The Deloitte team predicts that up to 40% of ICE component suppliers should be starting their transformation right now. “Their very existence is at stake,” is the way Deloitte puts it.

But change is expensive. It consumes personal energy, time, resources and finances. Steep declines in sales of new vehicles due to Covid-19 has resulted in rating agencies downgrading many suppliers, making it more expensive to borrow, according to research conducted by Roland Berger and Lazard. The company points out that the Covid-19 crisis is very different to that of the 2008/09 meltdown, which was followed by rapid recovery. “Lower vehicle sales in parallel with technological disruption will be the challenge for suppliers in the coming years” is the prediction. This is supported by the Deloitte team, which states: “when Covid-19 hit, we saw massive disruption in supply chains, production stops and slagging demand. This in turn caused companies throughout the automotive industry to take on even more debt. OEMs and suppliers are under pressure to optimize cash conversion and to invest in new business models at the same time. “Suppliers will therefore have to optimize their operations and evaluate the profitability of their respective plants across regions. But that may not be enough to quickly improve the balance sheets of this capital-intensive industry. Many companies will also have to look at divesting parts of the business or merging the top group”. Alarm bells should be ringing in the offices of politicians and authorities in the smaller vehicle producing centers. Subsidies and tariff barriers have combined to support automotive sectors which would not otherwise be viable. In the short term OEMS and Tier suppliers may be able to leverage the potential loss of jobs and technology to squeeze more concessions out of the governments wanting to retain their automotive manufacturing sector. But, unless the countries or regions create a unique competitive edge, the industry in its present form will never be self-sustaining without incentives and concessions – which many governments in developing economies will no longer be able to afford. The rapid switch to electric vehicles in the world’s biggest and most profitable markets adds another dynamic – the global Tier suppliers with plants in their countries will no longer be producing components for ICE vehicles, or will be able to meet demand more profitably using modern auto[1]mated plants situated close to the assembly line. So, adding to the growing list of challenges facing automotive leaders is the physical positioning of their plants. Roland Berger and Lazard predict that China and South America will continue to show growth, while new vehicle sales will stagnate in Europe, North America and Japan. Companies have to learn to get by on selling less. There are many more questions than answers – it is safe to say that only the well resourced, the adaptable and the lucky will be doing business the same way two years from now.

AUTOMOTIVE INDUSTRIES and Rutgers, the State University of New Jersey, have put together a digital library of back issues of AI from the early 1900’s (high res and low res) of approximately 230,000 images of the print publication. This archive, which documents the birth of the auto industry to the present, is available to AI subscribers. Go to AI’s homepage www.ai.com and click on the “AI Library” link or visitwww.ai-online.com/100YearLibrary

More Stories

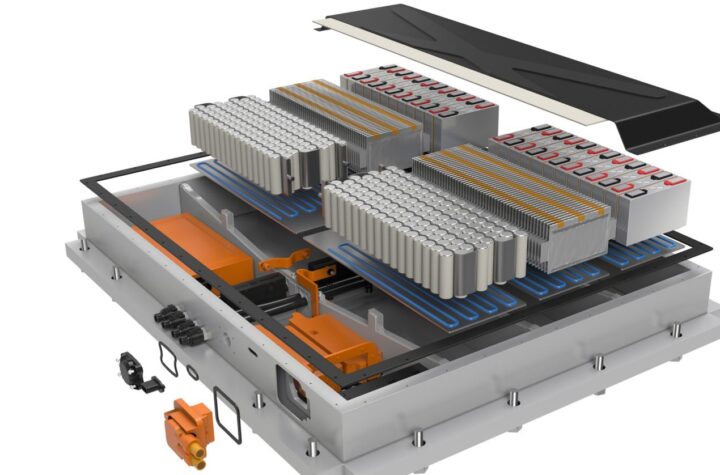

DuPont materials science advances next generation of EV batteries at The Battery Show

How a Truck Driver Can Avoid Mistakes That Lead to Truck Accidents

Car Crash Types Explained: From Rear-End to Head-On Collisions