To borrow from the wisdom of Yogi Berra, the one thing we do know for sure about 2013 and beyond is that “the future ain’t what it used to be”. The future that has changed is the industrial and consumer dominance of the West. Eastern manufacturers are now innovators setting the bench-marks for quality. We saw it first with Japan, then with Korea. In 2000 Hyundai Motors was bankrupt. Today it is one of the world’s fastest-growing car manufacturers, ranked around fifthlargest.

Chinese and Indian marques will undoubtedly follow suit. While all this means more choice for consumers, auto industry suppliers have seen what was once a neatly defined market served by a limited and stable number of manufacturers change fundamentally, along with their role: “As suppliers take on more responsibility for technology innovation, they will need to become more agile and adroit in managing the technology project portfolio,” says Booz & Co in its 2013 Automotive Industry Perspective. Booz & Co advises suppliers to rethink their approach to contracting with OEMs and become “more discerning” in their evaluation of programs.

For example, ask whether there is a clear path to recover costs for a given program. “To improve the chance that their innovations will fit seamlessly and hence improve competitive positioning, suppliers will need to continue to expand their knowledge of the vehicle systems in which they play.

This could involve enhanced networking or partnerships with sub-tier suppliers (such as electronics providers), market peers, or adjacent technologies, in addition to traditional OEM relationships,” says the White Paper. Where there does seem to be consensus among the various analysts is that – barring any unforeseen developments – vehicle sales will continue to grow, even in a depressed Europe. Consulting group Polk is among those which see a 6.6% growth in American light vehicle sales, to 15.4 million units, and reaching 16.2 million by 2015. What is uncertain is what Americans will be driving. The Polk White Paper observes: “Most dealers and leaders running key units within an OEM will continue to struggle with owner loyalty given the number of new model introductions hitting the market (over 40) and an aggressive marketing strategy being put into effect by virtually every OEM. With make-loyalty hovering around 48%, it means over half of any brand’s customer base will defect.

As Booz & Co point out, the challenge for suppliers is to tool up for the new models, and to have enough flexibility to absorb lower than expected sales as consumers switch brands, or to gear up if a model is selling faster than expected. With all the choice in the market-place, buyers will not wait around while a factory and its suppliers catch up with demand.

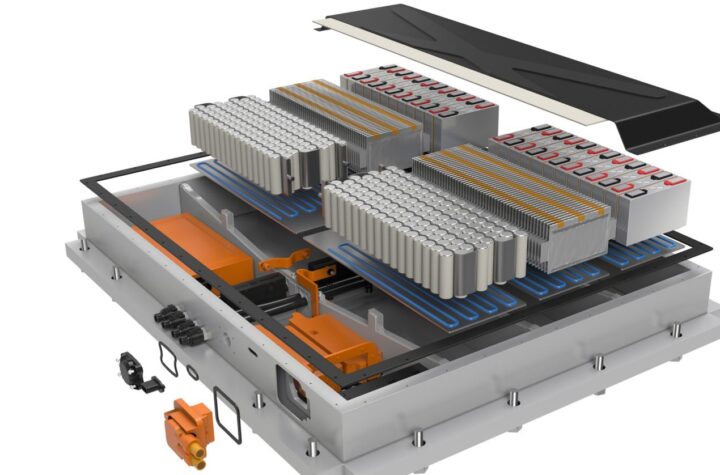

A good example of the risk is the switch to electric vehicles and hybrids, where improved efficiency in combustion engines is slowing the transition to electric power: Hybrids will continue to occupy less than 3% of the market due to “very affordable fuelefficient vehicles powered by none other than good ‘ol fossil fuel.

Sales of 4-cylinder vehicles broke 50% in 2012 in the U.S. and the sub-compact and compact car segment will be a focal segment in 2013,” predicts Polk.

Outside of the US, the market reflects the same challenges and opportunities. It is expected that Brazil, Russia, India and

China will account for over 60% of total global light vehicle sales growth between 2012 and 2020.

Polk sees the globalization of vehicle design presenting opportunities for aftermarket suppliers as vehicle components will increasingly become universal.

Booz & Co sums up the situation nicely: “The automotive industry is in a phase of both rapid and broad technological innovation that spans several scientific disciplines—chemistry (batteries), materials science (lightweight materials), and consumer electronics (infotainment). It’s becoming exceedingly difficult and too costly for OEMs to “go deep” across all technologies. Additionally, some nonautomotive players have superior specialized technical capabilities and R&D scale in specific disciplines. These factors are fundamentally shifting the industry’s long-standing model of innovation —which had been centered around large OEMs and major suppliers — toward a more decentralized approach in which OEMs serve as integrators, and large and small suppliers play an expanded role. All in all, for those suppliers with the foresight, flexibility and drive to succeed in the auto industry, the future is better than what it used to be.

More Stories

Automotive Industries (AI) Newsletter April 2025

GlobalLogic Pioneering Software-Defined Vehicles, AI Innovation, and Sustainable Solutions for the Future of Automotive Mobility

Cybord TCI – The Future of Manufacturing Integrity