Supply Crunch or Falling Demand? Dichotomies in the Semiconductor Market in 2H22

[Excerpt. Click to request access to full article]

By Rekha Menon-Varma, Managing Partner at Vertaeon

A multitude of factors contributed to a supply crunch in the semiconductor market late 2020 and 2021. These included the post-pandemic recovery, increasing demand in a supply-constrained setting, COVID-related impacts in Taiwan, Malaysia and Philippines, port congestions in China, and natural disasters. Multiple industry segments reliant on chips were impacted, including personal computers, consumer electronics, home appliances, and the automotive industry.

As the affected industry segments get back to the new operating equilibrium, we see mixed signals in the semiconductors markets. Depending on your industry, subsegment and geography, your experience could range between a glut or a crunch, and between an investment or capex reduction. We can see that an ongoing and comprehensive business risk assessment, complete with market-specific, financial, geopolitical, and macro indicators, is key to better-understanding and making decisions on these impacts.

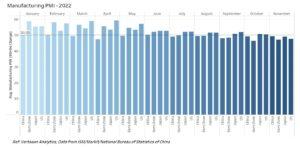

A key indicator of consumer sentiment, the new order PMI (purchasing managers index), shows demand falling across the board, stemming from inflation levels, interest rate hikes and the general economic climate. The manufacturing PMIs for the US, China, Japan, and Eurozone have fallen below 50 since November 2022, indicating an overall reduction in industrial production.

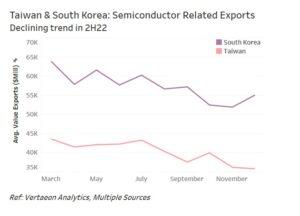

Global trade flows trended down in 2H22. Taiwan’s semiconductor export orders shrank in October and November, compared to 2021, partially due to weak consumer demand and impact from China’s zero-COVID strategy. South Korea had also been trending down but showed a slight uptick in December. It is also important to understand the impact of all the above changes on global trade flows, to develop a forward-looking perspective.

This makes sense when we pair it with corresponding projections for some end-markets; Semiconductor revenue from the PC and smartphone segments were reported to decline 5.4% and 3.1%, respectively, in 2022 per Gartner. However, semiconductor content per vehicle is projected to increase from $712 in 2022 to $931 in 2025 due to the transition to electric and autonomous vehicles. While there is a surplus of chips used in consumer electronics applications, the automotive sector seems to remain faced with a supply crunch.

Continued Supply Impacts on the Auto Industry

For starters, COVID-related production disruptions and natural disasters contributed to a sustained chip shortage in the automotive sector. Then, the Russia-Ukraine conflict put upward pressure on energy and raw material costs, especially in Europe. As semiconductor suppliers ramped up to meet rising demand post-pandemic, capex investments in 2022 hit record highs; however, they prioritized consumer electronics over the legacy chips used in automobiles. It was therefore not surprising that vehicle production was expected to be down by nearly 3.8M vehicles in 2022, more strongly impacting North America and EU. Carmakers like Toyota, Honda, Volkswagen, Ford, and Stellantis were among the impacted.

As a mitigation strategy, carmakers have been finalizing direct partnerships with chip manufacturers to secure semiconductor chip supply for their product-lines. This amounts to business model innovation, akin to those seen within the electric vehicle (EV) value chain, for high-value, functional chips.

On one hand, chip makers are facing potential excess inventory in 2023 due to other declining segments. On the other hand, they can allocate dedicated capacity for the auto sector, through either directly partnering with automakers or via increasing legacy chip supply through the value chain. As an example, Samsung Electronics, Yageo, and SK Hynix are three of the many switching their focus toward increasing automotive capacity.

Financial performance and investments in manufacturing for key semiconductor players – Tracking key performance indicators here suggests mixed signals. We have seen upticks in capital spending in 2021 and 2022 but planned reductions for 2023 in an attempt to cut expenses. While some players are investing in manufacturing infrastructure, others are implementing Capex reductions. Relative to financial performance, operating margins eroded in 2H22, and key operating ratios (asset and inventory turnover) also trended downward as 2022 closed as Vertaeon’s financial analytics shows.

Vertaeon continues to monitor macro, geopolitical and other key events which may persistently impact the automotive industry. Notables below, where geopolitics is reshaping both global operations and its footprint:

1. Investment commitments from Governments – Significant investment commitments have been made by governments, often with restrictions on global manufacturing. Examples include the $52.7B Chips and Science Act signed into law in the US in August 2022, the European Chips Act that aims to mobilize more than €43 billion of investments to swiftly respond to any future supply chain disruptions, and the $143 billion support package from China to support its semiconductor industry towards self-sufficiency in chips.

2. Impacts of restrictions associated with Government funding – These can impact the global supply chain model, affect the utilization of existing capacity in China, operating profitability, and access to local markets. Lastly, it would be important to map these restrictions to Capex commitments and the financial performance of the major players. Reshoring, friend-shoring, and near-shoring will come into play in 2023 in conjunction with offshoring.

3. Geopolitical Tensions– The continuing Russia-Ukraine conflict, and tensions between China and Taiwan, are both material to this topic and to leading suppliers from Taiwan. US Commerce Dept. initiated trade controls in September and October of 2022 to limit sales of advanced chips and technologies to China and has placed 36 companies to an entity list as of December 2022. In addition, the Netherlands and Japan may adapt some of the US export controls.

Conclusion:

There are some business implications for customers of semiconductors(i) Pricing and bargaining power may be better with increasing chip inventories (ii) Delayed capex investments can cause another potential supply shortage as interest rates and a potential recession threat slow down (iii) Semiconductor suppliers to and in China will be more closely monitored and (iv) Semiconductor companies utilizing US or EU subsidies will have to invest regionally.

The outlook for 2023 is sober for most semiconductor players, with less spent on capital projects and better inventory management. However, modest revenue growth is still expected in most end markets. Within the automotive industry, business model innovations, advancements in technology features, and EV growth would contribute to this. Overall, chip supply is expected to improve, but geographically, tensions may be higher as some of the measures set in motion in 2022 get implemented. Geopolitical and macro trends will play a key role not just in how the semiconductor market fares, but also, by extension, how the automotive and other customer industries are impacted.

(To request this article in its entirety, reach out to us at brandon.mckc@vertaeon.com)

Author: Rekha Menon-Varma is Managing Partner at Vertaeon LLC, a risk and strategy analytics firm. She has extensive expertise in strategy, enterprise risk and digital transformation. Rekha has 20+ years of experience in automotive and industrial value chains. Rekha holds MS in Chemical Engineering from Auburn University and MBA from The Wharton School, University of Pennsylvania.

Author thanks the Vertaeon team including M. Cheng, A. Lawrence and B. Crooks for support in preparation of this article.

Disclaimer: The content in this blog is intended for informational purposes only. Multiple published sources were used as references. Vertaeon provides no endorsement and makes no representations as to accuracy, completeness, or validity of any information or content on, distributed through or downloaded, or accessed for this article. All rights and credit go to original content owners from various sources. No copyright infringement is intended. Vertaeon will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All information is provided on an as-is basis without any obligation to make improvements or to correct errors or omissions. Vertaeon makes no guarantees or promises regarding the sources and does not necessarily endorse or approve of their content. You may contact Vertaeon at https://www.vertaeon.com with any questions.

Copyright © 2023 Vertaeon LLC. All rights reserved.

More Stories

What to Expect From Your First Visit to an Injury Law Office

Best ATV for Farm Work and Best UTV for Ranch Owners

UnitX Launches The World’s Fastest to Deploy AI Smart Camera to Bridge the Manufacturing Vision Gap